By Eamonn Ives (Research Director, The Entrepreneurs Network).

Executive summary

Abundant energy supplies are essential to economic growth – energy use and economic output are not only tightly correlated but also have a bidirectional, causal relationship

But the threat of climate change and the subsequent need for decarbonisation means that countries must work out how to radically reshape their energy systems – away from being dependent on fossil fuels, and towards clean alternatives

In practice, this will see economies steadily ‘electrify’ – with electricity becoming the energy vector that is overwhelmingly responsible for powering homes, transport and industry

This will necessitate the generation of far greater quantities of clean electricity – with forecasts suggesting a doubling from 300TWh to 600TWh per year, or possibly more in more ambitious scenarios

To match this increase in demand, we will need to rapidly accelerate the construction of new energy assets that can provide it

Nuclear energy – as the only proven, scalable, reliable clean power source – is perfectly poised to deliver the additional capacity required

That’s why Britain has been targeting a significant expansion of nuclear energy, including from novel technologies like small modular reactors (SMRs) – and ensuring the long-term security of the sector was explicitly pledged in the most recent Labour manifesto

But without comprehensive reform to how nuclear power stations can be built, this effort will be made needlessly more difficult – adding time and expense to the rollout of new nuclear reactors for no good reason

Failure to make it easier and cheaper to construct new nuclear projects like SMRs will lock us into an expensive and potentially unreliable energy system, and delay the already stretching timelines for grid decarbonisation

Businesses will be rendered less competitive relative to those in economies with abundant supply, and lucrative energy-intensive industries such as AI will think twice about basing operations in the UK

Policy proposals

More sites should be opened up to SMR development, recognising the fundamental differences they have compared to gigawatt-scale nuclear plants

Local authorities which approve the construction of new nuclear power stations should be entitled to capture more of the business rates they pay

Regulators must be adequately resourced to enable swift decision making processes on new nuclear assets

Britain should mutually recognise the work of nuclear regulators in other allied countries when it comes to approvals for new nuclear designs

The time it takes for all clean energy projects to receive consent should be shortened

Clean power acceleration areas that exempt the construction of clean energy assets from environmental impact assessments should be introduced

FOREWORD

The UK target of Net Zero by 2050 is one we must meet. Thankfully, after significant work by the private and public sectors, we can see credible delivery pathways that are now feasible and affordable. This is something that looked almost impossible just a decade ago. Nuclear – and in particular the roll-out of small modular nuclear reactors (SMRs) – can be a key part of that journey.

SMRs offer safe, reliable and clean baseload capacity based on proven technology. Most importantly, they can be delivered significantly more quickly and efficiently than ‘large’ nuclear reactors. If deployed as part of a fleet, they also allow for iterative learning and innovation.

Holtec Britain – where I am a Senior Adviser – plans to invest £1.8 billion into the UK to deliver SMRs domestically and for export to MENA. This includes £1.5 billion to build a new advanced SMR factory in South Yorkshire, creating more than 1,600 highly-paid jobs, with a further 14,300 across our wider UK programme. Doing so will also create a £30 billion export opportunity for the UK over the decade. Building on the government agreements in place, we have brought together a team of experts from the UK, US and South Korea to ensure we learn from global best practice.

Energy is the lifeblood of modern economies. It underpins every aspect of societal advancement and economic growth. Historically, energy consumption, carbon emissions and economic output have been clearly linked. But as we move away from fossil fuels and towards low carbon energy sources and greater energy efficiency, we can continue to see growth, but with far lower negative impact on the environment.

The potential of SMRs extends beyond supplementing our energy mix. They enable a vision of decentralised, resilient energy systems that can support a wide range of applications – from providing stable power in industrial clusters to ensuring energy security in remote locations. They also can provide a major export opportunity for the UK.

However, despite progress in recent years and renewed support and commitments from the new Secretary of State, realising the full potential of SMRs requires further concerted action on multiple fronts. This important policy paper sets out some potential avenues for the government to explore. They include reforming regulatory frameworks to reduce barriers, ensuring adequate resourcing of regulatory bodies, and importantly, working towards mutual recognition with key international partners on safety and design standards.

As we urgently navigate the complex landscape of energy transition, we need all the technologies and policy levers available, not only to achieve Net Zero but also ensuring that being a clean energy superpower brings jobs, economic growth, and opens up new export markets. This is our opportunity to build on our manufacturing history and to re-industrialise parts of the UK with new, highly-paid green jobs. The ideas in this paper will help us to do that.

Prof Dame Julia King FREng FRS FMedSci, Baroness Brown of Cambridge – Senior Adviser, Holtec Britain

Introduction

Late one night in January 2014, astronauts aboard the International Space Station peered out of a window and took what would instantly become an iconic photograph. Four-hundred kilometres below was the Korean peninsula – and while its southern half was bathed in the warm glow of artificial light, the north was shrouded almost entirely in darkness. The reason why is a dramatic demonstration of the relationship between energy consumption and economic growth. South Korea has an economy verifiably measured in the trillions of dollars, North Korea has one roughly estimated in the billions.

Though this example might be the most vivid, and admittedly a rather simplistic, display of the importance of a dependable supply of energy for economic success, the lesson it presents holds true even in less extreme circumstances. As illustrated by Chart 1, below, an extraordinarily tight correlation can be observed between energy consumption per capita and economic output per capita.

What’s more, academic research has shown that more than being merely correlated, there is a causal relationship between energy consumption and economic growth. Further still, the causality is bidirectional – in other words, not only do more economically developed countries consume more energy, more energy consumption actively drives further economic development as well.

The interplay between energy use and economic flourishing should hardly come as a surprise. The Industrial Revolution, which more than anything else in history was what hauled much of humanity from grinding poverty, was built on the harnessing of new energy sources in the form of fossil fuels. Once we began converting dormant chemical energy in coal and oil into useful kinetic energy with combustion engines, living standards rocketed. Earnings per capita in the UK doubled from the start to the end of the 19th century, before then quintupling over the 20th.

Box 1. The importance of Energy Return on Investment (EROI)

Energy Return on Investment (EROI) is a way to measure the efficiency of exploiting any given energy source. It compares the amount of energy delivered by an energy source to the amount of energy it takes to ‘harness’ that energy source – in other words, how much energy it takes to convert or capture an energy source and turn it into useful energy which anyone can readily use.

EROI is usually expressed as a ratio. For example, if one unit of energy is invested to extract, refine, and deliver oil, but that process returns 25 units of usable energy from the oil, then the EROI of that oil source is 25:1. The higher the ratio, the more energy surplus and greater return on the initial energy investment. A low EROI, such as one at or close to 1:1, would essentially signal the process involved is only just breaking even energywise. An EROI of less than that would represent an energy sink – with more energy being expended than was eventually returned.

EROI is a crucially important concept because it allows for the comparison of the net energy profits of different energy sources. The higher an energy source’s EROI, the more excess energy it provides to power economic productivity, technological advancement and improve living standards beyond just operating the energy sector itself.

No single EROI ratio exists for each different energy source, as they will be context dependent. Some natural gas reserves will be easier to tap than others, for example, just as solar panels closer to the equator will capture more sunshine than those at more northern or southern latitudes. By and large, however, economies progress when EROIs are higher rather than lower.

Only when people have ready access to cheap and reliable energy can a cornucopia of goods and services be produced. Industries such as steel making, aviation, and chemicals and fertiliser production would be utterly unviable in the absence of abundant energy supplies. Indeed, we should never lose sight of the fact that the availability of energy is often the single limiting factor behind much of what is possible in society. In many cases, we already have the technologies required to deliver a far better world – it is just that the energy required to power them is prohibitively expensive. Lowering the cost of that energy would bring just about everything closer within our grasp – from cheaper transport to warmer homes, to even more imaginative things like geoengineering or interplanetary travel. In a sentence, energy abundance should rank much more highly in the priority lists of governments around the world.

Other considerations pertinent to the energy system have also risen up the agenda of late.

Despite alternative energy sources making impressive inroads of late, the global energy system overwhelmingly remains dominated by fossil fuels – coal, gas and oil supplied over 137,000TWh of primary energy in 2022, versus less than 27,000TWh from wind, solar, nuclear and hydropower. And while the burning of these fossil fuels supplies great quantities of useful and dependable energy, it also generates harmful greenhouse gases – 37.15 billion tonnes of carbon dioxide in 2022 – and other environmentally harmful pollutants too. In order to halt climate change and improve air quality, it is necessary to curb their emission on a global scale. International agreements such as the Paris Accord and the Glasgow Climate Pact obligate governments worldwide to take steps to decarbonise their economies, and the energy system is often one of the most obvious and important places to start. In the UK, the new Labour government has just come to power with a manifesto commitment to entirely decarbonise the power supply by 2030.

Energy security has also emerged as something that governments need to take much more seriously. Recent geopolitical crises and exogenous shocks like the Covid-19 pandemic sent energy markets into a tailspin, with enormous swings between excess energy supply and excess energy demand. Energy prices spiked in 2022 to such a degree that the British Government felt obliged to cushion household and industrial energy bills, at a cost of several tens of billions of pounds to the public purse. In order to prevent similar catastrophes happening in the future, a spectrum of voices have argued that greater supplies of homegrown energy are required.

A suite of technologies will enable the transition to a cleaner, more efficient, more secure domestic energy system. One thing that is obvious from the outset, however, is that electrification – whereby electricity becomes the primary means to power transport, heating systems and other household appliances, and even industrial processes – will be pivotal. While mass electrification will see us consume far less gas and oil, we will need to produce far more electricity to replace them. By some estimates, the quantity of electricity required in Britain could double from around 300 terawatt-hours (TWh) annually today to around 600TWh by 2050. If we want to be even more ambitious about economic growth, and play host to emerging energy-intensive industries such as artificial intelligence, sustainable aviation fuel and decarbonised steel production that figure could – and indeed should – be even higher.

In order to do this, more electricity generation capacity will be required. One novel form of generation which has captured the attention of policymakers of late is small modular nuclear reactors (SMRs). These power stations do exactly what they say on the tin – they’re:

Small – typically with a nameplate capacity of around 300 megawatts or less, as compared to gigawatt scale reactors such as those at Hinkley Point C with capacity of 1,600MW;

Modular – in other words, produced on a repeated basis, to benefit from economies of scale in production, as well as in construction and then in operation and maintenance;

Reactors – they harness nuclear fission reactions to generate electricity.

One of the primary rationales for SMRs is the idea that they could be delivered more quickly and less expensively than conventional, gigawatt-scale nuclear power stations. This is precisely what is required if we are to build the capacity we require to decarbonise the electricity grid in line with our legal commitments, as well as ensuring new industries have the power supplies they need to function. It was no surprise, therefore, to see the Labour manifesto explicitly pledge to back their development in the UK.

Yet despite the increasing awareness that SMRs can help the UK to achieve a cleaner and more resilient energy system, policy issues and a lack of urgency stymie their path to deployment – and it is not expected that a single SMR will be supplying electricity to the grid until at least the early-2030s.

We can speed that timeline up. This research briefing investigates what those policy issues are, and how we might reasonably create a policy framework more conducive to the construction of SMRs in Britain. Only by having an energy system which is abundant, clean and reliable can entrepreneurs flourish and get Britain’s economy growing at a rate we can be proud of once again. The new Labour Government has set itself a commendable mission to make the UK a clean energy superpower, and the policies we set out in this report would help it to deliver on that goal.

Britain’s energy system – past, present and future

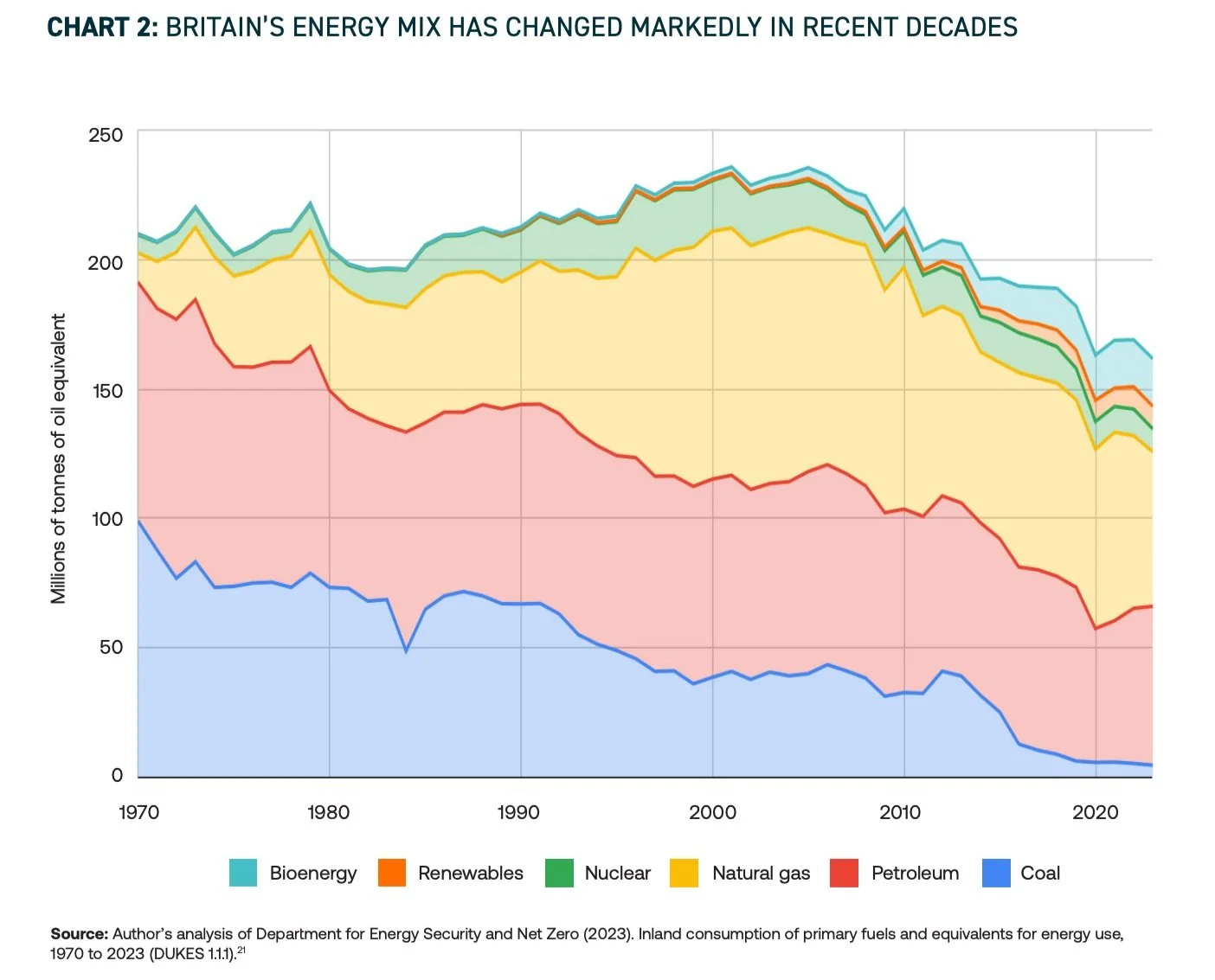

Britain’s energy system has undergone dramatic changes in recent decades – as illustrated in Chart 2, which shows where we get our primary energy from by fuel source. Slowly but surely, new energy sources such as wind and solar power are supplying ever more of our energy demand. Our fossil fuel dependency is gradually reducing, down from 97% in 1970 to 77% in 2023. As well as a changing energy composition, we are also consuming less energy in total now than we did previously – energy consumption peaked in 2001, at 237 million tonnes of oil equivalent (Mtoe), and has since fallen to 164Mtoe.

In the grand scheme of things, Britain has a well functioning energy system. There’s dependably gas in our boilers, petrol in our fuel pumps, and electricity is only the flick of a switch away. In 2023-23, the reliability of supply for the National Grid was 99.999997%. As illustrated by Chart 3, the carbon-intensity of our electricity has been slashed over time too, especially in the past decade thanks largely to the near total retirement of coal fired-power stations from the generation mix and the rise of renewables. In 2023, 162 grammes of carbon dioxide were produced for every kilowatt hour of electricity, the least carbon-intensive year since reliable records began.

With all that being said, there decidedly is room for improvement, while other challenges loom on the horizon. The biggest of these is undoubtedly the fact that the energy system of the future will be dominated much more by electricity as the primary energy vector, as opposed to gas and oil. As noted before, because of the need to electrify the economy, we will consume far less of the latter and far more of the former.

This additional load will come from a variety of sources. Renewables will play a vastly expanded role, with the new Labour Government aiming to quadruple offshore wind capacity to 55GW and triple solar capacity to 50GW by 2030. All the recent evidence of renewables build-out rates should give us a great deal of hope that achieving these targets will be eminently feasible – deployment forecasts for renewables are consistently beaten, with more and more renewable capacity being added each year than was previously imagined possible. A large part of this is due to the staggering reductions in price that both solar and wind power have experienced, as the technology underpinning them improves, and production and supply chain maturation enables cost savings.

Yet, while renewables will undoubtedly play a critical role in the energy system of the future, we must recognise that they are not without limitations of their own. The most obvious of these is that no matter how sophisticated they become, turbines will only rotate when the wind is blowing, and photovoltaic panels will only work when the sun is shining.

The supply and demand of electricity on the National Grid is balanced at half hourly ‘settlement periods’, and data is available on how much each energy source of electricity is supplying the grid at any one point. Every year there are 17,520 settlement periods (two per hour, 48 per day, 336 per week, and so on), but during 6,064 of those in 2023 (or 35% of the time), wind and solar contributed less than 25% of the overall power supply. Chart 4, below, shows how erratic renewable energy can be.

Moreover, where this intermittency really becomes problematic is when renewables generation is depressed for long time periods. For instance, for nearly five consecutive days at the start of March 2023, renewables generated less than 25% of the electricity supply. (And indeed, between 2pm on 26 February and 10.30pm on 9 March, renewables only contributed 25% or more of the electricity supply for 39 hours).

At present levels of renewables penetration on the grid, intermittency doesn’t represent too much of a fatal flaw (together, wind and solar produced 96TWh, or 32%, of the total 296TWh of electricity supplied in the UK in 2023). Any gaps in generation caused by low wind speeds or low solar irradiance can be filled in relatively easily by ramping up gas-fired power stations. However, this obviously comes at a cost – both in terms of the money that needs to be spent having gas-fired power stations acting on standby, and in terms of the contribution they make to climate change and air pollution. As we pivot through from high-carbon electricity mix, to a low-carbon electricity mix and eventually towards an entirely carbon-free electricity mix, unabated gas-fired power stations will become less of an option to call upon, and that presents issues for system reliability.

Of course, it is not as if this problem has escaped the minds of the renewables industry – far from it. Solutions to reducing and ultimately ending intermittency are being worked on with results already paying dividends. One of the primary avenues to address intermittency is to couple renewables with clean energy storage, such as batteries, which turn wind and solar effectively, if not inherently, into reliable clean power sources.

Yet while there are ample grounds to believe battery technology will improve in the coming years – as it has done enormously in previous decades – it would represent an enormous gamble for a country like Britain to think it can rely on batteries to adequately smooth out supply and demand mismatches, especially where there is a power generation deficit of more than a couple of days. The largest existing battery-energy storage system – Vistra Moss Landing in California – can supply 3GWh, only enough to power perhaps 53,000 average British homes for a week (and that is even before they switch to electric heating, charging electric vehicles and so forth). As such, other forms of clean energy generation must not go ignored by policymakers (and as we shall see in the following section, they are not).

That encapsulates the main future challenge for our energy system. But as mentioned previously, other problems are already biting, chief among which is the high cost of electricity in Britain relative to other countries.

Given how important electricity is as an input cost to virtually all economic activity, this necessarily impinges on our competitiveness and living standards. Entrepreneurs frequently tell us how high energy costs are a barrier to their growth. Moreover, lack of supply could render the United Kingdom unviable for energy intensive sectors, or sectors where a dependable supply of electricity is essential. Historically this would be industries such as manufacturing, but nowadays it would also include emerging and critical sectors such as data centres and artificial intelligence (AI), both of which consume vast quantities of electricity.

As noted by the International Energy Agency earlier this year: “After globally consuming an estimated 460TWh in 2022, data centres’ total electricity consumption could reach more than 1,000 TWh in 2026. This demand is roughly equivalent to the electricity consumption of Japan.” Hyperscalers like Microsoft, Google and Amazon – and hopefully future hyperscalers we are not yet aware of – know that they need reliable and significant power supplies. And they are putting their money where their mouths are. As was reported by The Financial Times in February this year: “Microsoft said last year it would buy nuclear power to cover up to 35 per cent of the energy needs of one of its Virginia data centres, when wind and solar power is not available.” Meanwhile, Amazon Web Services recently spent $650 million to acquire a site directly powered by the adjacent Susquehanna Steam Electric Station, a 2.5GW nuclear power plant. AI expert Leopold Aschenbrenner describes the scene in America: “[T]here’s a fierce scramble to secure every power contract still available for the rest of the decade, every voltage transformer that can possibly be procured [...] By the end of the decade, American electricity production will have grown tens of percent.”

If Britain wishes to capture a slice of the market share in these lucrative industries, which will doubtlessly form an increasing proportion of the future global economy, as well as having important security ramifications, firms need to be confident that they will have reliable access to competitively priced electricity. They will not invest in countries which cannot supply them with the power they need – instead, investment, and the associated jobs and tax revenues, will flow elsewhere. And the opportunity cost does not just apply to tech companies which are most obviously dependent on cheap and reliable electricity. All businesses benefit from lower energy costs, especially if it makes them more competitive on the global stage.

In summary, in years to come, Britain’s energy system will need to overwhelmingly transform into simply being an electricity system. This narrowing of the energy ‘base’ will necessitate the generation of much more electricity – perhaps twice as much as is currently the case, but possibly even more if Britain wishes to compete, as it should, in emerging industries such as AI, sustainable aviation fuel and decarbonised steel production. Renewables will play a vital role in generating much of this additional electricity demand, but in the absence of inexpensive, long-duration energy storage capacity, there are good reasons to believe that a renewables-only strategy for power supply is risky, certainly in the medium term, and even possibly in the long term too. For this reason, other forms of electricity generation must be on the table. In the next section, we will explore what one of those might be.

The nuclear option – the case for SMRs in the energy system

Nuclear power is the only proven zero-carbon, reliable and scalable power source that has been deployed anywhere in the world. Nuclear energy is also one of the safest forms of power generation in terms of deaths per kilowatt hour of electricity generated, and its involvement in the global energy system has avoided several tens of gigatonnes of carbon dioxide in recent decades. A one inch pellet of uranium contains the same amount of energy as 17,000 cubic feet of natural gas, and it’s thanks to this that a single nuclear reactor can supply more power than a wind farm covering hundreds of square miles. Modern nuclear power stations also have anticipated lifespans of around 60 to 80 years, whereas a wind turbine may last only 25.

Despite carrying all the hallmarks of being a miracle fuel, however, Britain’s recent legacy on nuclear power is mixed.

Things began very positively. In 1956, Calder Hall in Cumbria made history by being the first full-scale nuclear power station in the world to supply electrons to a civilian energy grid. After that, 18 further nuclear power stations were constructed. But the most recent of those – Sizewell B in Suffolk – was connected to the grid nearly 30 years ago, in 1995. No fewer than eight Prime Ministers have moved into 10 Downing Street since it opened. In the same time frame, South Korea has switched on 18 brand new nuclear power stations.

Worse still, many of the nuclear power stations that had been constructed prior to Sizewell B are now nearing the end of their lifespans, or have already been retired. Thirty-six reactors have been shuttered in the UK, wiping almost 8GW of clean, reliable capacity from the grid. Of the nine reactors currently operational in Britain, eight are slated for decommissioning by 2028, with the other due to close not long after in 2035. This will roughly see a further 6GW of clean, reliable electricity generation capacity vanish from Britain’s energy system.

Numerous issues have combined to create this state of affairs. But the overarching problem has been the failure to build out nuclear capacity in a programmatic way. Projects have been characterised by stop-start processes, with little in the way of continuity and long-term certainty. This drives up the costs for developers – and indeed all companies in the nuclear industry supply chain – who cannot be sure that investments they made in R&D, staff training, capital equipment and so on will pay off if future projects dry up.

Of course, to a certain degree, heterogeneity is a good thing. Different designs and approaches to construction can theoretically drive learning and innovation through competitive forces. But there are aspects particular to the nuclear industry where greater standardisation could be desirable. Whether the UK specialises in pressurised water reactors (PWRs) as opposed to boiling water reactors (BWRs), for instance, will have implications for the future export potential of British designs, and indeed fuel supply as well as its subsequent safe disposal. Given PWRs are the most widely adopted commercial reactor technology across the world, is best suited to speedy deployment, and is the technology where global competition is most intense, there are strong justifications for the UK to prioritise them over BWRs.

Some good news for Britain’s future nuclear landscape is admittedly on the horizon. Hinkley Point C (HPC) in Somerset is currently under construction, and, when completed, its two 1.6GW reactors will supply around 7% of Britain’s electricity demand. Plans to construct a near replica of HPC – Sizewell C – are also in advanced stages – which would add an extra 3.2GW capacity to the grid. The completion of these two sites will make up for capacity that will be lost over the coming years. In one regard, this is welcome – but in another, it simply represents Britain’s energy system standing still.

Yet there are further grounds for optimism on rolling out more nuclear power. First and foremost, among the British public, attitudes towards nuclear power have shifted noticeably in recent months, from slight net opposition to clear net support – as can be seen in Chart 6, below.

In terms of policy, there have been changes too. In 2022, the previous Government unveiled the British Energy Security Strategy (BESS), in which a target to increase nuclear capacity in the UK to 24GW by 2050 was laid out. Meanwhile, last year Sir Keir Starmer described nuclear power as a “critical part” of Britain’s energy mix, and the recent Labour manifesto specifically stated that “Small Modular Reactors will play an important role” in bolstering the energy supply.

The interest in SMRs from policymakers comes with good reason. As mentioned previously, SMRs are reactors with generating capacity of around 300MW or less, and are constructed in a modular fashion – with parts prefabricated in an external factory and then assembled later on site. This confers a number of advantages, including:

Standardisation – the mass-production of components means that companies manufacturing, assembling and eventually operating SMRs can benefit from economies of scale, innovation and learning-by-doing, thus bringing down costs over time;

Reduced risk – with lower chances of overrunning costs or construction timelines, SMRs are less risky, which is especially important in terms of the affordability of raising capital to finance their development, and opens up the possibility for more entirely privately financed projects;

Faster timeline to generating – compared to gigawatt-scale nuclear power stations, SMRs can be built faster, allowing projects to feed into the grid, displacing fossil fuelled power generation, and begin generating revenue sooner as well;

Decentralised energy supply – due to their smaller scale, there is greater ability to strategically locate SMRs closer to where power is demanded, such as an industrial cluster, which lowers transmission costs and strengthens the energy system overall by not concentrating generating capacity within a handful of sites;

Export potential – SMRs could be exported around the world to more locations (such as those which may not require gigawatt-scale reactors), representing a potential jobs boon for a country which establishes itself as an SMR market leader;

Increased competition – with over 80 SMR designs being developed around the world, there is scope for a high degree of competition between providers, which theory dictates will spur innovation and drive down costs further.

With all of this in mind, it is therefore unsurprising that successive governments have thrown such weight behind developing SMRs in Britain in recent years. And this support hasn’t come simply in warm words and stretching targets. Hundreds of millions of pounds of taxpayer money has been made available to advance the development of SMRs. For example, in the 2021 Net Zero Strategy, a £210 million Future Nuclear Enabling Fund (FNEF) was announced, which aims to “help mature potential nuclear projects ahead of the expected government process to select the next nuclear projects.” As of April 2024, three companies – Holtec Britain Limited, GE Hitachi and Cavendish Nuclear – had collectively been awarded nearly £67 million from the FNEF.

The growing appreciation of the role that nuclear power – and SMRs in particular – should play in Britain’s future energy system ought to be welcomed. The previous Government should be given credit for creating policy frameworks which enable nuclear developers to bring forward plans to construct new assets in Britain, as should the new Labour Government for promising to see through the development of SMRs. Yet, as we shall explore in the following section, there is still further to go. Fundamentally, no SMRs currently exist in the UK, despite the potential to bring them online. Without adequately fixing other regulatory issues, there’s good reason to believe that Britain’s nuclear rollout will not be possible at the envisaged timescales and cost estimates. This represents the squandering of scarce resources, delays the decarbonisation of the economy, and keeps the country exposed to the vagrancies of the international energy system which have driven up energy costs so precipitously in recent years. If we are to maximise Britain’s nuclear future, further policy reforms will be required.

Box 2. Types of nuclear reactor

There are different ways to classify the various distinct designs for nuclear reactors – from the type of reactions they are based on, to their ‘generation’, to the type of coolant used. Below, five main types of reactors by coolant are briefly described.

Pressurised Water Reactor. The most common form of nuclear reactor around the world today is the Pressurised Water Reactor (PWR). This design accounts for around 70% of the global reactor fleet and works by utilising a primary cooling loop that circulates water through the reactor core and a secondary loop where steam is produced to power the turbine. The water in the primary loop is kept from boiling by maintaining high pressure within the reactor. The water in the secondary loop is under lower pressure, allowing it to boil and thus spin the turbine, which generates electricity.

— Boiling Water Reactor. Boiling water reactors (BWRs) are the second most prevalent type of reactor worldwide, comprising about 15% of the global reactor fleet. In contrast to PWRs, BWRs use a single loop where water is kept at a pressure that permits boiling to occur. The steam that is produced in the reactor is sent directly to the turbine, where it spins and generates electricity.

— Pressurised Heavy Water Reactor. Pressurised heavy water reactors (PHWRs) are the third most common reactor type, accounting for 11% of the global reactor fleet. This design employs heavy water, a distinct form of water, to manage cooling and control nuclear reactions. The use of heavy water enables the reactor to utilise natural uranium as fuel, in contrast to the enriched uranium required in PWRs and BWRs.

— Gas-cooled reactor. Gas-cooled reactors (GCRs) are a less common type of nuclear reactor, typically making up a small portion of the global reactor fleet. These reactors use a gas, such as carbon dioxide or helium, as the coolant to transfer heat from the reactor core to the steam generators. The high temperature of the gas allows for efficient heat transfer, and the design often incorporates graphite as a moderator to slow down the neutrons. The generated steam then drives the turbine to produce electricity.

— Molten-salt reactors. Molten-salt reactors (MSRs) are an advanced and much less conventional type of nuclear reactor. In MSRs, the nuclear fuel is dissolved in a molten salt mixture, which serves both as a coolant and a medium for the nuclear reactions. This liquid fuel allows for continuous operation and easy removal of fission products. The heat generated in the molten salt is transferred to a secondary loop, where it can be used to generate steam and drive a turbine to produce electricity. MSRs are praised for their potential safety advantages and efficient fuel use, as well as their flexibility in using various types of nuclear fuel.

Different reactor designs confer different advantages and disadvantages. For example, while BWRs are simpler in design due to their single-loop system, they have the downside relative to PWRs of the steam passing directly through the reactor core, which means that the turbine components are exposed to low levels of radioactivity. This can complicate maintenance and increase operational costs. MSRs are highly regarded for their ability to eliminate the nuclear meltdown scenario because the fuel mixture is kept in a molten state.

Moreover, there can be advantages to having a single reactor type within a country. In the UK, in order to domesticate fuel production and have a consistent used-fuel disposal strategy, a sufficient number of PWRs may be required.

Policy recommendations – How to enable faster and cheaper construction of new nuclear assets

Much work is already underway to improve the policy landscape pertinent to the construction of new nuclear power stations in the UK. In this section, we outline a handful of further policy reforms which could ensure that Britain is as attractive a proposition as possible to nuclear companies wanting to develop and build SMRs within our shores.

The proposals are geared around enabling quicker and cheaper development of new nuclear assets, which would confer benefits to British taxpayers and businesses alike. It is worth reiterating the case for why speed is of the utmost essence here.

First, SMRs for civilian power are still a nascent development. No country as yet enjoys an entrenched reputation as being a world leader in deploying the technology – meaning that the chance to become one is still very much up for grabs. If Britain were to get its policy framework fit for purpose, it has every chance to become recognised as the go-to place for SMR expertise.

Second, we are undoubtedly at an inflection point in economic history – with new technologies like AI and other digitally enabled industries rapidly reshaping the global economy and world of work. Decarbonisation of industrial processes, commodities like steel, and sustainable aviation fuel will also be critical going forwards. All of these sectors require reliable and significant quantities of electricity, and will not locate themselves in countries where they are not confident they can access it. The swift deployment of SMRs, co-located with data centres and other energy-intensive premises will be crucial for capturing a share of the future market in these industries.

Third, with the election of the new Labour Government, the importance of taking robust action on climate change has been restored to its rightful place. If we are to meet our legally binding Carbon Budgets, and credibly remain on track to reach Net Zero emissions by 2050, we must accelerate the deployment of clean energy technologies. Not only this, but we will also need to electrify other aspects of the economy – from industry, to aviation, to transport, to agriculture. For this to be possible, again, access to significant and dependably quantities of electricity will be paramount. SMRs can allow us to do this, and also confer the advantages of being able to bring power online more quickly – and thus displace what would otherwise be electricity generated by fossil fuelled-power stations.

1. More sites should be opened up to SMR development, recognising the fundamental differences they have compared to gigawatt-scale nuclear plants

It goes without saying that before you can build a nuclear power station, you first need to find somewhere to put it. The current specific planning regime for energy infrastructure projects in the UK is set out in the energy National Policy Statements (NPS), with nuclear being covered by EN-6. However, EN-6 was designated over a decade ago in 2011, listing only eight sites that the government deemed potentially suitable for gigawatt-scale nuclear power stations to be developed on. Since then, the nuclear industry has moved on considerably – not least in the advancement of SMRs – but the government has failed to keep pace.

Fortunately – if somewhat belatedly – the previous Government recently took steps to rectify the situation. In January 2024, a consultation into siting beyond 2025 (when EN-6 expires) was launched. In the Civil Nuclear Roadmap, the Department for Energy Security and Net Zero stated: “To reach our ambitions for nuclear power by 2050, we believe that additional sites beyond those designated in the EN-6 NPS will be required for nuclear power stations, along with greater ongoing flexibility in the site selection process to enable new technologies.” This wording was encouraging, and set in motion the journey to a more permissive approach to opening up more sites to nuclear development. We would certainly recommend the new Labour Government honours this direction of travel, and, at the bare minimum, declares that any site previously deemed appropriate for nuclear development should be open to developers to build SMRs on.

But in order to fully reap the potential that SMRs promise, we must also be proactive in the search for more sites. For SMRs to be a success, and able to contribute a meaningful amount of power to the grid, many more areas for development will be required. One obvious starting point would be former industrial sites or those of other retired power stations. Brownfield areas like these will generally be well suited to SMR development – as they will likely be close to energy-intensive businesses, or with infrastructure already in place to enable a quick connection to the grid.

Research from the US Department of Energy has suggested that 80% of former coal mining sites are suitable for the deployment of an advanced reactor, smaller than a gigawatt in capacity, and there is no reason to think that this couldn’t translate across to the UK. (Indeed, President Biden recently signed into law legislation known as the ADVANCE Act, which requires the US nuclear regulator to develop a pathway to enable the timely licensing of microreactors and nuclear facilities at brownfield and retired fossil-fuel energy generation sites).

Britain should look to this for inspiration, and follow suit accordingly. A future siting regime for nuclear power must ensure that new sites become available for SMR construction to happen on them, with a priority being former industrial sites and other brownfield land.

2. Local authorities which approve the construction of new nuclear power stations should be entitled to capture more of the business rates they pay

A perennial reason for why Britain fails to build the infrastructure it needs – whether energy, transport, commercial or residential – is because of the split incentives in terms of who bears the costs and who reaps the benefits of new construction. Local authorities, for instance, are often under pressure to block developments, because it is in their rational self-interest to appease existing voters even if this prevents growth which creates new jobs and generates additional tax revenues.

Understanding this set of affairs, the logical policy response should be to find ways to enable local authorities to capture more of the benefits of approving developments, to make up for the negative impacts of construction. Reforming how business rates work offers a quick and easy way in which to do this.

Business rates are a tax on non-domestic properties. They are levied annually on a property’s ‘rateable value’, and then multiplied by a national multiplier – currently typically 54.6% in England, 49.8% in Scotland, 56.2% in Wales and 29.02% plus a sub-regional rate of between 25.57% and 38.2% in Northern Ireland. Thus, a non-domestic property in England with a rateable value of £100,000 will be liable to pay £54,600 in business rates each year.

Since 2013, local governments have been able to retain up to 50% of the business rates collected in their area – meaning in the previous example, £27,300 would go to the local authority. As economists Sam Bowman and Ben Southwood point out, however, if we enabled local authorities to retain a greater share of a property’s annual business rates contribution it would considerably swing the incentives for approving developments in favour of new construction. Importantly, this would not result in any lost tax revenues. Rather, it would only change who retains the same lump sum of tax – the local government or national.

Aligning the incentives in favour of development will be critical for getting decisionmakers’ approval for the construction of new infrastructure assets like SMRs and the things they might eventually power – such as data centres, which will be necessary for the future world of work. We believe allowing local authorities to retain more of the business rates these developments will eventually pay is an elegant way to get more construction approved. Enacting this change could be done without primary legislation, and should be a priority for the new Government to bring in.

3. Regulators must be adequately resourced to enable swift decision making processes on new nuclear assets

When the House of Commons Science and Technology Committee launched an inquiry last year into expediting the delivery of new nuclear assets, one of the more prominent issues that came up was the lack of capacity within regulators responsible for developing new sites – namely the Office for Nuclear Regulation (ONR) and the Environment Agency (EA). In its written evidence to the inquiry, the EA said: “Recruitment and retention of regulatory resources are already under pressure from a range of factors including industry demand and uncompetitive salaries. This should be addressed to ensure that the competency and capability of regulators can meet the demands of the new build programme.” As noted in the same inquiry and as has been mentioned to us during our research for this report, salaries for regulators tasked with approving development plans can vary wildly: “The disparity within nuclear regulation resources can be seen directly in the salary bands offered. The lowest grade Environment Agency nuclear regulator (band N1a) salary range begins at £50,001, whereas the equivalent salary band (band 3) at the ONR would start at £71,033.”

In 2022/23, the ONR spent a little over £44 million on salaries, up only slightly from 2021/22. Since then, however, there has been a considerable step-change in ambition for nuclear power development, which is reasonable to assume will increase workload for the ONR.

In light of the step up in ambition, we recommend that a thorough review is undertaken to ensure regulators are appropriately resourced to deliver on this. Moreover, consideration for greater flexibility in pay between regulators, which recognises the importance of approving new nuclear assets, should be given. At the same time, the government should also consider what could be done to make such increased resourcing contingent on the delivery of solid results. If we remain stuck in a malaise, with approvals for new nuclear projects stuttering, we should not be afraid to withdraw newly allocated resources.

4. Britain should mutually recognise the work of nuclear regulators in other allied countries when it comes to approvals for new nuclear designs

At the 2022 Autumn Statement, the former Chancellor Jeremy Hunt received widespread praise from various different quarters for announcing that he would be commissioning a Pro-innovation Regulation of Technologies Review, to advise how Britain can better regulate emerging technologies. Ahead of the 2023 Spring Budget, Sir Patrick Vallance, the then Chief Scientific Adviser and leader of the Review at the time, presented interim findings on the life sciences portion of the Review. Among the recommendations it made – and which was ultimately accepted and implemented by the previous Government – was the proposal to allow the Medicines and Healthcare products Regulatory Agency and the National Institute for Health and Care Excellence to adopt a broader approach to the mutual recognition of products already approved by trusted international partner organisations, particularly for well-established technologies. Put more succinctly, where medicines and healthcare tech have been approved by regulators in like minded countries, they should benefit from quicker or even automatic approvals processes in the UK too.

This same policy approach should be used for nuclear reactors as well. Where reactor designs have already been approved by countries with high standards for nuclear regulation, the ONR should likewise grant automatic approval for that reactor to be deployed in the UK. As infrastructure expert Sam Dumitriu has highlighted, this would enable reactors like KEPCO’s APR-1400, which forms the backbone of South Korea’s most recent nuclear power expansion, to get approval in the UK without having to go through approximately four years of approvals processes. (The APR-1400 has already proven to be extremely reliable, and South Korea’s nuclear fleet experiences losses to capacity at a rate of about a seventh of the UK’s. As such, it is hard to think of any good reason for not allowing its construction in Britain.)

Not only would adopting a faster approvals process enable new nuclear power stations to be built more quickly, it would also free up resources within the ONR. With this additional newfound capacity, regulators could focus on scrutinising less tested designs – such as those for SMRs, and other innovative reactor-types – which truly should warrant closer inspection. This could allow the ONR to emerge as a world-leader on approving novel reactor designs, allowing Britain to become an attractive location for developers to test the next generation of nuclear reactors.

As well as pursuing unilateral mutual recognition, Britain should also lead on efforts in international fora – such as at the IAEA and COP climate conferences – to broker agreements on further regulatory harmonisation between countries. This would be all the more important if the UK was to steal a march in SMR production, as this could become a significant export opportunity for companies based in the UK which are designing and manufacturing them.

5. The time it takes for all clean energy projects, not just offshore wind, to receive consent should be shortened

In its most recent Infrastructure Progress Review, the National Infrastructure Commission gave a withering review of Britain’s planning system: “Currently the planning system constrains the roll out of infrastructure at the pace that is required. The past decade has seen average times for nationally significant infrastructure projects increase significantly. Planning costs are rising and uncertainty in the system has increased.” It also noted that the planning system for Nationally Significant Infrastructure Projects, while working well when initially introduced in 2008, has declined in effectiveness in recent years, with consenting times increasing by a staggering 65% between 2012 and 2023.

In the BESS, the previous Government acknowledged that the planning system is inhibiting the rollout of clean energy infrastructure. It noted that development and deployment of offshore wind farms can still take up to 13 years, for instance, and accordingly made a pledge to cut that process time in half. One of the ways singled out to achieve this was to reduce the time it takes for projects to get consent from four years to one. More details of this ambition were set out in the Offshore Wind Environmental Improvement Package, which was legislated for as part of the Energy Act 2023.

The ambition displayed and action taken to reduce the time it takes for offshore wind to gain consent is admirable, and shows that governments are eminently capable of delivering positive policy change at pace in response to serious challenges. But it is curious why the measures only apply to one form of clean energy generation and not others. Similar initiatives should be introduced for all forms of clean power, including nuclear and solar.

6. Clean power acceleration areas that exempt the construction of clean energy assets from environmental impact assessments should be introduced

Last year, the European Commission proposed revisions to the long-standing Renewable Energy Directive in order to speed up the rollout of clean power generation. One of the flagship amendments to the Directive was to create a duty for member states to establish ‘renewable acceleration areas’. Renewable projects in these areas would benefit from simpler permitting processes and shorter timelines, as well as not having to complete steps such as undertaking environmental impact assessments.

As expert planning lawyer Mustafa Latif-Aramesh explains: “projects located in renewables acceleration areas are proposed to benefit from accelerated administrative procedures, including a ‘tacit agreement’ in case of a lack of response by the competent authority on an administrative step by the established deadline; in effect, a non-response is a deemed consent.” Thus, he continues: “Rather than having to show there are no likely significant effects [to environmental outcomes from an infrastructure project], authorities will have to have ‘clear evidence’ to consider that a specific project is ‘highly likely’ to give rise to such significant unforeseen adverse effects. Again, the absence of such a statement is a green light.”

Not only should Britain follow in the footsteps of our European allies, it should go further still – establishing ‘clean power acceleration areas’, which would also include nuclear energy as an eligible form of power generation. This would give Britain a comparative advantage for the construction of clean energy assets, drawing in investment and creating well-paying, skilled jobs.

Of course, it is imperative that protections for nature in and around sensitive areas like Sites of Scientific Interest and Areas of Natural Beauty should be maintained. But, outside of areas like this, environmental rules which block or even just decelerate the build-out of clean power generation do little to help biodiversity – in fact, it means that we lock ourselves into a power system more carbon-intensive than it needs to be, exacerbating climate change, which itself is a key driver of biodiversity loss on a global scale.

7. ‘Turnkey’ terms should be explored as a way of scaling SMR development in the UK at speed

Given SMRs are still very nascent, it is understandable that the Government may be reluctant to make any big bets on a particular technology or delivery model at this stage. To date, the Great British Nuclear competition has been an effective way to walk the line between not commiting to a single pathway, while still giving a range of providers sufficient incentive to carry on developing their propositions.

This is wise – for example, Advanced Modular Reactors (AMRs) based on Generation IV pressurised water technology are at an earlier stage of development, but promise improvements over Generation III+ PWRs (the current generation close to commercialisation like Holtec’s SMR-300, Rolls Royce SMR or WEC UK’s APR300). Even within Generation III+ there are some differences, which is why it is right for the Government to hedge bets at the development stage.

Another key aspect governing the likely ease, speed and cost of deployment is the delivery model. Again, since SMRs have not yet been deployed at scale, there is little data to go on when assessing this question. However, it is worth noting that the spate of reactors built in the US in the 1960s which kick-started the nuclear industry there were all built under ‘turnkey’ contracts. Under such a contract, the manufacturer agrees to design, build and test a reactor for a pre-agreed price before ‘turning over the key’ to the project owner, thus assuming all the delivery risk.

Today, very little gigawatt-scale nuclear capacity is delivered in this manner given the known risks, but as has been extensively discussed in this report, these risks may not apply to SMRs – as their production is done on a repeated basis, benefiting from economies of scale and, crucially, fewer unknown unknowns which have recently plagued large-scale nuclear projects since each is a unique and hugely complex undertaking.

As such, the turnkey model of delivery stands out as one which SMRs could particularly benefit from, at least initially in order to incubate the industry and demonstrate the viability of SMRs as a component of the overall energy system.

conclusion

Advanced economies need reliable access to energy. Competitive economies need reliable access to cheap energy. And all economies need reliable access to clean energy if we’re to successfully halt climate change. Nuclear energy presents a way of providing all three of these.

Britain started its nuclear journey with promise – building the first civil nuclear reactor, and several more in quick succession. But then came its nuclear construction drought. Skills were lost, supply chains collapsed, and other factors conspired to thwart Britain’s nuclear industry.

The good news is that we finally seem to be rounding a corner. The new Labour Government has made a bold and ambitious commitment to delivering clean power by 2030, and recognises the role new nuclear developments must play in providing that. Meanwhile, sites are progressing at Hinkley Point C and Sizewell C, and there has been an eruption of interest in new nuclear technologies, such as SMRs. While they should have come sooner, actions taken by the previous Government should also give encouragement that Britain stands on the cusp of a nuclear renaissance.

Public and private money is poised to be deployed in the construction of SMRs from a variety of companies. In order to make that construction as efficient, timely and cost-effective as possible, there are further steps the new Labour Government should now take – including improving the regime for siting, aligning permission incentives for local government, properly resourcing regulators and recognising the work of international allies in granting approvals.

Nearly seven decades ago, Britain could credibly claim to be a world-leader with respect to civil nuclear power. Sadly, after years of dither and delay, it could not say the same today. But with the right frameworks in place, there’s every reason to think we could quickly turn things around, and emerge as a pioneer in the nuclear technologies of tomorrow.

As energy expert Eli Dourado wrote for us last year in our essay collection Operation Innovation: “Literally and figuratively, energy is the fuel that drives the engine of entrepreneurship the world over. It is embedded into just about everything of value that we build and consume. Societies which demonstrate the capacity to most successfully harness energy are invariably those which best flourish. With a little more research and development, and a lot more deployment, we can ensure that an ever increasing share of the global population has the means to fulfil its true innovative potential.” These words ring truer today than ever before – and the time for making good on them is now.

acknowledgements

Support for this paper came from Bradshaw Advisory – an economics, policy and public affairs consultancy helping clients navigate, influence and solve public policy challenges.

The author would also like to thank all of the individuals who reviewed previous drafts of the research and provided constructive feedback, especially Jan Zeber at Bradshaw Advisory. Any errors of fact or judgement are the author’s alone.

For the full verison of the report, click here.